Mortgagequestions is the Official web portal of PHH Mortgage that has been created for Customers who want easy and comfortable Payments on their Mortgages and Loans. PHH Mortgage is a Non-Bank Mortgage Company that has been in the Business Since 1984. PHH Mortgage is now the Division of the Ocwen Financial Corp, which Purchased the Lender’s Parent Business in the Year 2018.

Borrowers may Normally get preapproved in one Business Day and those who don’t have a Credit History may be able to Use some of the Additional options including a record of on-time paying bills, to demonstrate trustworthiness. The PHH Mortgage Company’s Headquarters are Located in Mount Laurel, New Jersey. Through the Mortgagequestions.com official web portal, Customers can check their Payment History, Interest or Tax Rates, and many other services.

About Mortgagequestions

When it comes to Mortgages, Loans, or Taxes or Satisfy their Doubts related to Mortgage or Loans, All Customers from the United States of America are able to Use the Mortgagequestions official Web Portal Services to pay off Due Payments.

The Company is also Known for Providing Various Mortgage Options, Including the Forty Years Fixed-Rate Loan. the official Mortgagequestions Portal is available for its Customers to make easy Payments and offers a range of various Payment Options. There are a lot of Customers in the United States of America Who Use the Services of the Mortgagequestions.com Portal to pay their Monthly Mortgage Installments.

Customers can also ask Questions and inquire about the Remaining Taxes, Installment, or Payment History as well as anything related to Mortgages or Loans. Mortgagequestions is a Web Portal that is dedicated to Comfortable Paying off Loans and Mortgages. You are able to get all the Queries or Questions related to Mortgage escrow, Loan Payments, Interest Rates, History of Payment Made, Tax Rates, PMI, or Modes and Methods of Auto Payments of Loans and Mortgages.

Features And Benefits of Mortgagequestions

All the Customers are able to get Access to Account Information 24/7.

- Customers can Review Payment and Statement History.

- Easily Request Support for Your Online Account.

- Get the Helpful Account Alerts in the Message Center.

- Get Registered in the Paperless Delivery for the Statements And Enjoy the Free Online Payments.

- Good Range of Fixed-rate Conventional and Government-Backed Loans.

- The Official Website Provides very Useful resources like calculators, checklists, and Instructive Materials.

Requirements For Mortgagequestions Login & Sign Up

In Order to complete the Mortgagequestions Login at the official Website, these things are needed:

- Mortgagequestions official web portal.

- Mortgagequestions Login Username, SSN, Email Address, and Password.

- Secure Internet Browser.

- PC, Laptop, Smartphone, or Tablet with Reliable Internet Access.

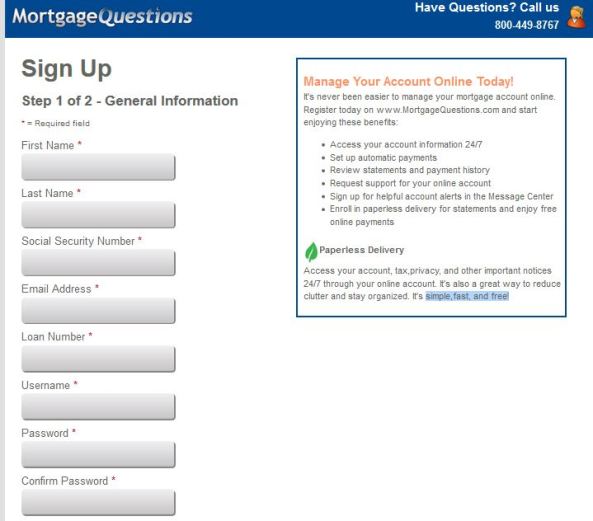

Mortgagequestions Sign Up And Registration Process

PHH Mortgage Offers the www.mortgagequestions.com official website to Customers in order to Enable them to Access their Accounts and Make PHH Mortgage Online Payments easily. In Order to Sign Up at the Mortgagequestions.com Official Web Portal, the Users need to Access the Mortgagequestions official website and then click on Register for Online Access. Here Below we have provided the Complete Step by Step Process For the Mortgagequestions Registration:

- STEP I: At First, Customers Need to Open the Secure Web Browser and Type https://www.mortgagequestions.com/main/.

- STEP II: Now You will be redirected to the Mortgagequestions Main Page from where You can see the “Register Now” Link.

- STEP III: Now You have to Tap on the Link that says Register Your Account, which is available on the Login Form.

- STEP IV: Now You have to Provide Your First Name, Last Name, SSN, and Your Property ZIP.

- STEP V: After Providing all these Details You have to Submit Your Bank Account Details.

- STEP VI: Now Submit Your Email Address and Mobile Number and Press the Register Button in order to complete the Registration Process.

- STEP VII: After successfully registering your Account You are able to easily Login into Your Account by just providing your Login Details.

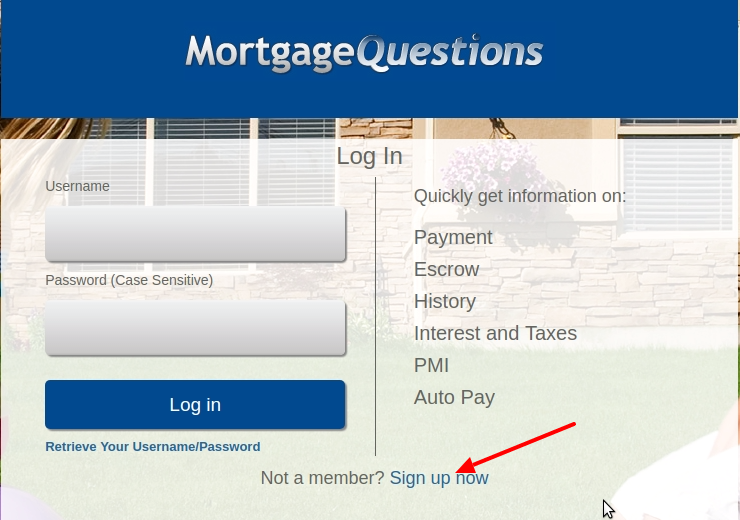

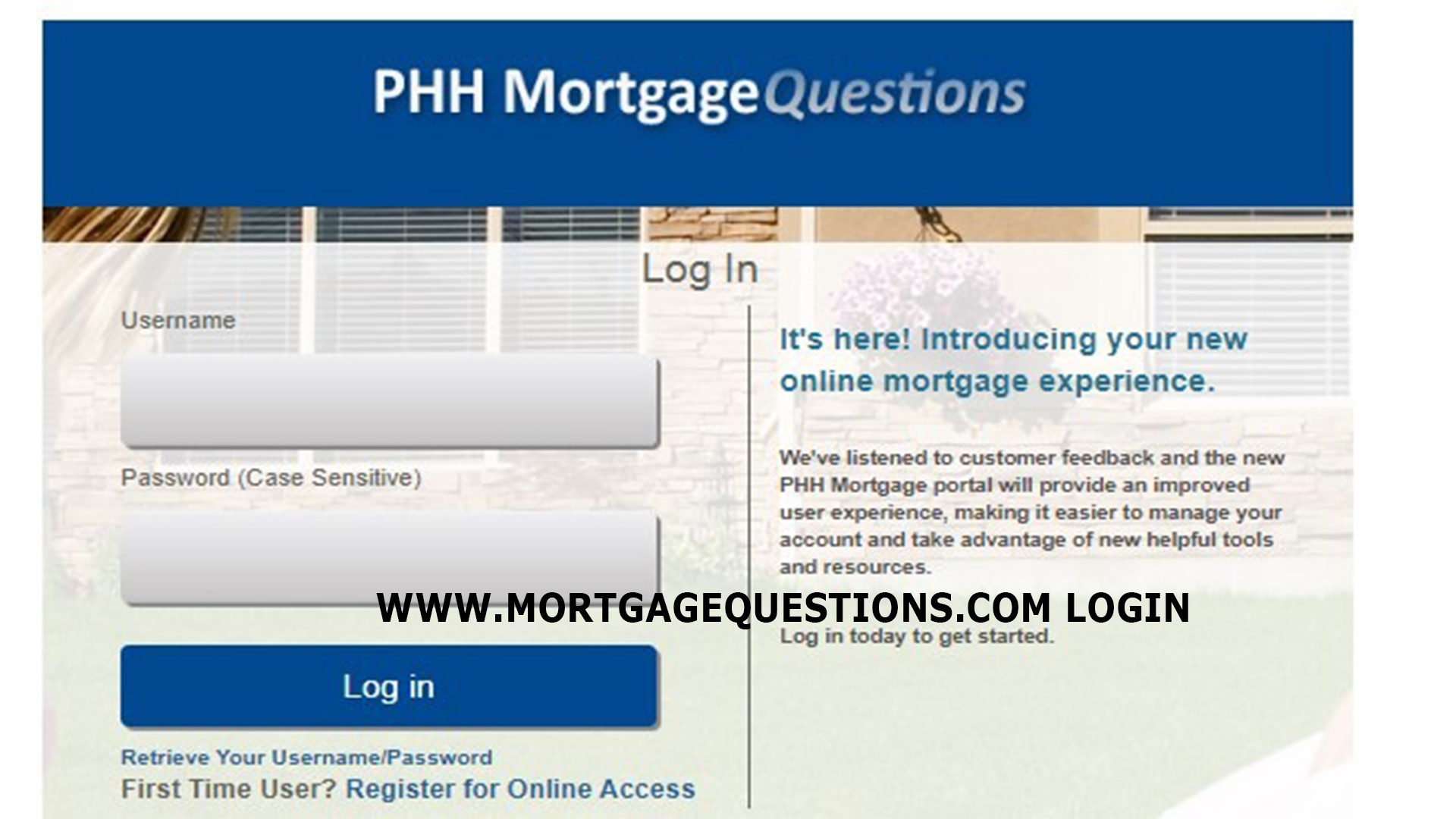

Mortgagequestions Login And Sign In Step By Step Process At www.mortgagequestions.com

If You have received a Loan from PHH Mortgage then You can Make a Payment by Visiting their official website at www.mortgagequestions.com. After visiting its official platform You are able to Check your Loan Status, Get Online Benefits, Make online Bill Payments, and Much More. In Order to log in at www.mortgagequestions.com, a User needs to access its official website, Click on the Login Link, and Access Your Online Account. Here Below is the complete Step by step-by-step process for Mortgagequestions Login at www.mortgagequestions.com:

- STEP I: At First Go to the official website of the Mortgagequestions at www.mortgagequestions.

- STEP II: Now Enter Your Login Details such as your Username and Password in the Given provided fields.

- STEP III: After Providing all the necessary Login Details You will be redirected to the Dashboard of the Website through which You can Check your Loan Status, Get Online Benefits, and Make online Bill Payments by clicking on the Mortgage Payment Section.

How to Reset Your Mortgagequestions Password?

If You have Forget Your Mortgagequestions Login Password then You can easily Reset it by accessing its official website. Here Below is the complete step-by-step Guide to Reset Your Mortgagequestions Login Password:

- STEP I: At First, Visit the official website of Mortgagequestions at www.mortgagequestions.com.

- STEP II: Now Click on the “Forget Password” Link, available on the Homepage of the Website.

- STEP III: Provide Your Email Address, Username, and SSN Number in the given fields.

- STEP IV: Now Click on the Recover Button, In order to Reset Your Mortgagequestions Login Password.

How to Reset Your Mortgagequestions Username?

In Case You have to Forget Your Mortgagequestions Login Username then You can easily Reset it by accessing its official website. Here Below is the complete step-by-step Guide to Reset Your Mortgagequestions Username:

- STEP I: At First, You have to Visit the official website of Mortgagequestions at www.mortgagequestions.com.

- STEP II: Now Click on the “Forget Username” Link, which is available on the Homepage of the Website.

- STEP III: Now You have to Provide Your Email Address and SSN Number in the given fields.

- STEP IV: Now Click on the Recover Button, In order to Reset Your Mortgagequestions Username.

How To Make PHH Mortgage Payments Online?

In Order to Make a PHH Mortgage Online Payment, You Must visit the Mortgagequestions Login Website. After Successfully logging in to the Mortgagequestions.com web portal, You need to Make Online Payments by clicking on the Mortgage Payment Section. Here Below is the complete Step by Step Process For Mortgagequestions Online Payment:

- STEP I: At First Visit the official website of the Mortgagequestions at www.mortgagequestions.

- STEP II: Now You need to Provide Your Login Details including your Username and Password in the Given fields.

- STEP III: Now access your Mortgage Payment option and carry out the payment by date and amount.

- STEP IV: The Money will be deducted from Your Bank Account which you have already provided at the time of Mortgagequestions Registration.

Mortgagequestions Customer Support Details

In Case If you have any problems regarding PHH MortgageQuestions, then You need to contact its customer service for assistance via:

For General Servicing Inquiries Toll-Free Number Is:

1-800-449-8767

For Website Support Toll-Free is:

1-833-862-0732

- Monday through Friday, 8:00 a.m. to 9:00 p.m. Eastern Time

- Saturday, 8:00 a.m. to 5:00 p.m. Eastern Time

General Mail

PHH Mortgage Services

P.O. Box 5452

Mount Laurel, NJ 08054-5452

Payment Addresses

Mortgage Accounts

PHH Mortgage Services

P.O. Box 94087

Palatine, IL 60094-4087

HELOC Accounts

PHH Mortgage Services

P.O. Box 0055

Palatine, IL 60055-0055

Requests for Information and Notices of Error:

PHH Mortgage Services

P.O. Box 66002

Lawrenceville, NJ 08648

Final Verdict

That’s All Related to Mortgagequestions, Sign Up, Login, Online Payments, and Customer Service. If You have any questions or queries related to Mortgagequestions then feel free to comment in below comment box. You can also get help from Mortgagequestions Customer Support Representatives by dialing its Toll-Free Number.

Frequently Asked Questions (FAQs)

Question 1: Are Mortgagequestions Safe and Secure?

Answer: Yes, Mortgagequestions is an official website for PHH Mortgage Borrowers. This Website is completely Safe and Secure and one can visit its official web portal to access their loan info, and status, make payments, and more.

Question 2: Why Mortgagequestions Website Prompting me to Verify the Account?

Answer: If You Access Your Account from the New Device or Browser then This Website may Request You to Verify Your Account before Logging in. For this, You need to select the most convenient way to receive the Verification Number to validate Your Access and Benefit from these enhanced Security Features.

Question 3: How To Pay My PHH Bill At Mortgagequestions?

Answer: You can easily Pay Your PHH Bill Online by just Signing into Your official website at www.mortgagequestions.com and redirecting to the Payment Section. You can also Pay Your PHH questions bills by Contacting Customer Care Over the Phone or Paying by Mail.

Question 4: Will I be able to Register At Mortgagequestions Using an International Phone Number?

Answer: Yes, If You are using the International Phone Number then You can still Register On the Mortgagequestions.com Website. However, Use Your Email Address to Authenticate Your Online Account instead of Your International Phone Number.

Question 5: I am Using the Mortgagequestions Mobile App, Do I need to Register separately at the Application?

Answer: No, If You are already Registered at Mortgagequestions.com Website then the Same Username and Password will Work on the Mobile App. But If You have not Logged in Before then You need to Register First.